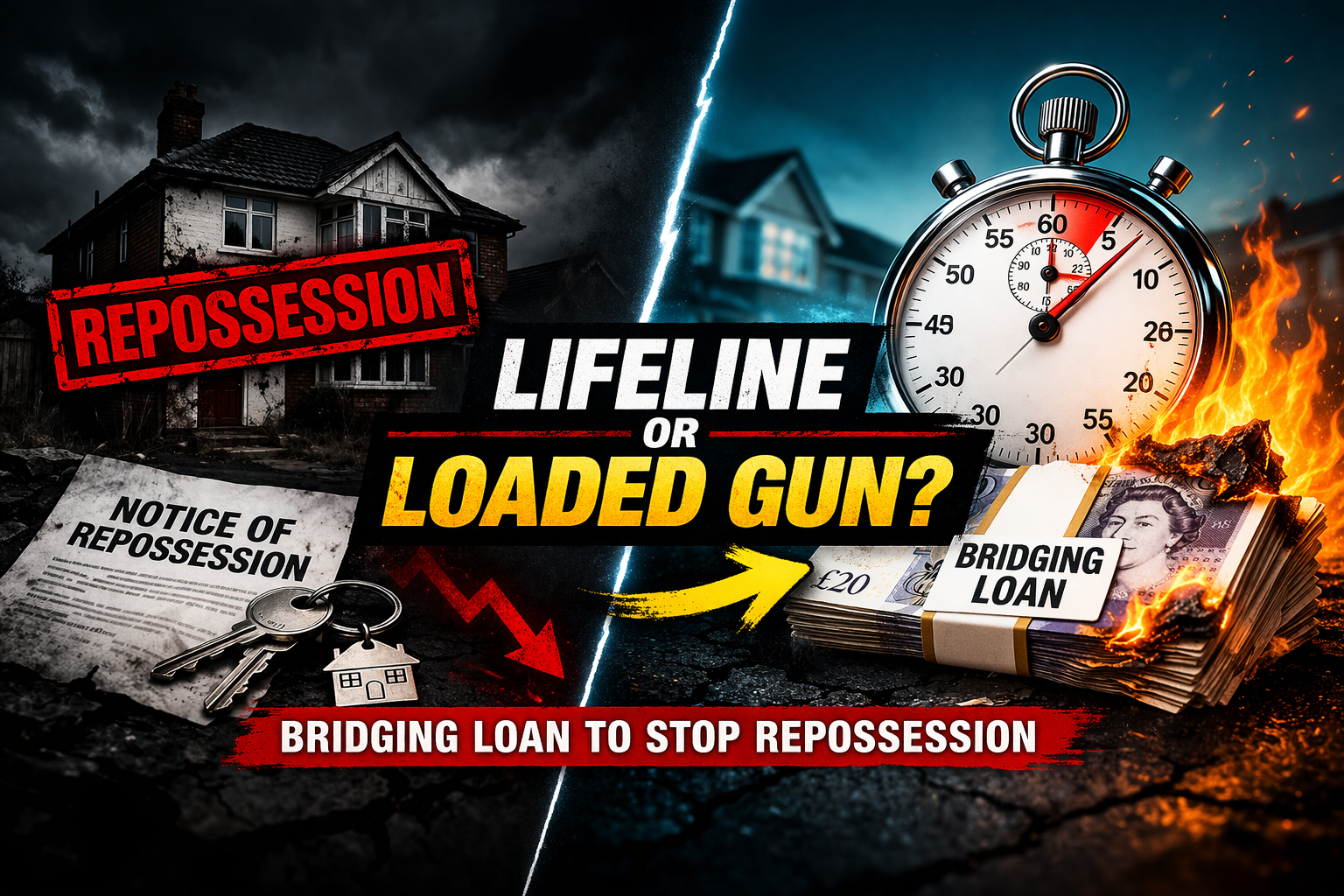

Bridging to Stop Repossession: Lifeline or Financial Suicide?

A bridging loan won’t save your property.

It buys you time — at 1%+ per month — to either fix the problem… or make it worse, faster.

The Reality Nobody Wants to Admit

When a repossession letter lands, most people panic.

They don’t build a plan — they grab the fastest money available and call it a solution.

That’s where bridging comes in.

Fast. Flexible. Expensive.

But here’s the part nobody tells you straight:

Bridging is speed — not salvation.

If you don’t have a real exit (sale or refinance you can actually deliver), you’re just swapping one problem for a bigger one.

One lender chasing you → now two

Arrears → plus interest, fees, and deadlines

Stress → multiplied

And that “we’ll refinance later” plan?

In this market — with arrears, missed payments, or a messy credit file — it’s often fantasy.

Most lenders want:

clean credit

stable income

track record

If you don’t have that, your real exit is usually one thing:

👉 Sell the property.

What Actually Happens (No-BS Breakdown)

Speed

Yes — bridging can complete in 5–15 working days.

But:

Legal delays kill deals

Court dates don’t wait

Bailiffs don’t care about your broker

👉 If you’re late — bridging won’t save you.

Cost

That “from 0.99% per month” headline?

That’s for perfect deals.

If you’re in trouble:

Expect 1.1% – 1.6% per month

That’s 13%–20%+ annually

Before fees.

Hidden Damage

Here’s where people get burned:

Arrangement fees (1–2%)

Broker fees

Legal fees (both sides)

Exit fees

Default interest if things slip

👉 You’re not buying time cheaply — you’re renting it at a premium.

The Brutal Truth

A repossession is bad.

A failed bridging loan + repossession?

That’s worse.

You’ve:

delayed the inevitable

increased your debt

damaged your credit further

And now you’ve got even less room to recover.

When Bridging Actually Makes Sense

There are cases where it works:

You already have a serious buyer lined up

The property is priced to sell fast

Title is clean, no legal mess

You’ve got a clear, realistic timeline

👉 Then bridging is a tool.

Not a gamble.

When It’s a Terrible Idea

Be honest with yourself.

If this is you:

“I’ll refinance later somehow”

“The market will pick up”

“I just need more time”

You’re not solving the problem.

You’re delaying it — at a cost you can’t afford.

What You Should Do Instead

If you’re facing repossession:

Get real on numbers — today

Speak to a broker who isn’t selling you hope

Price for a fast sale, not a perfect one

Protect what equity you still have

Because once it’s gone — it’s gone.

Bottom Line

Bridging can save a deal.

It rarely saves a bad situation.

👉 If your exit isn’t solid, bridging isn’t a strategy.

It’s a countdown.

If you’re in this situation — or heading towards it — don’t guess.

Drop me a message or book a call.

I’ll tell you straight what your real options are.